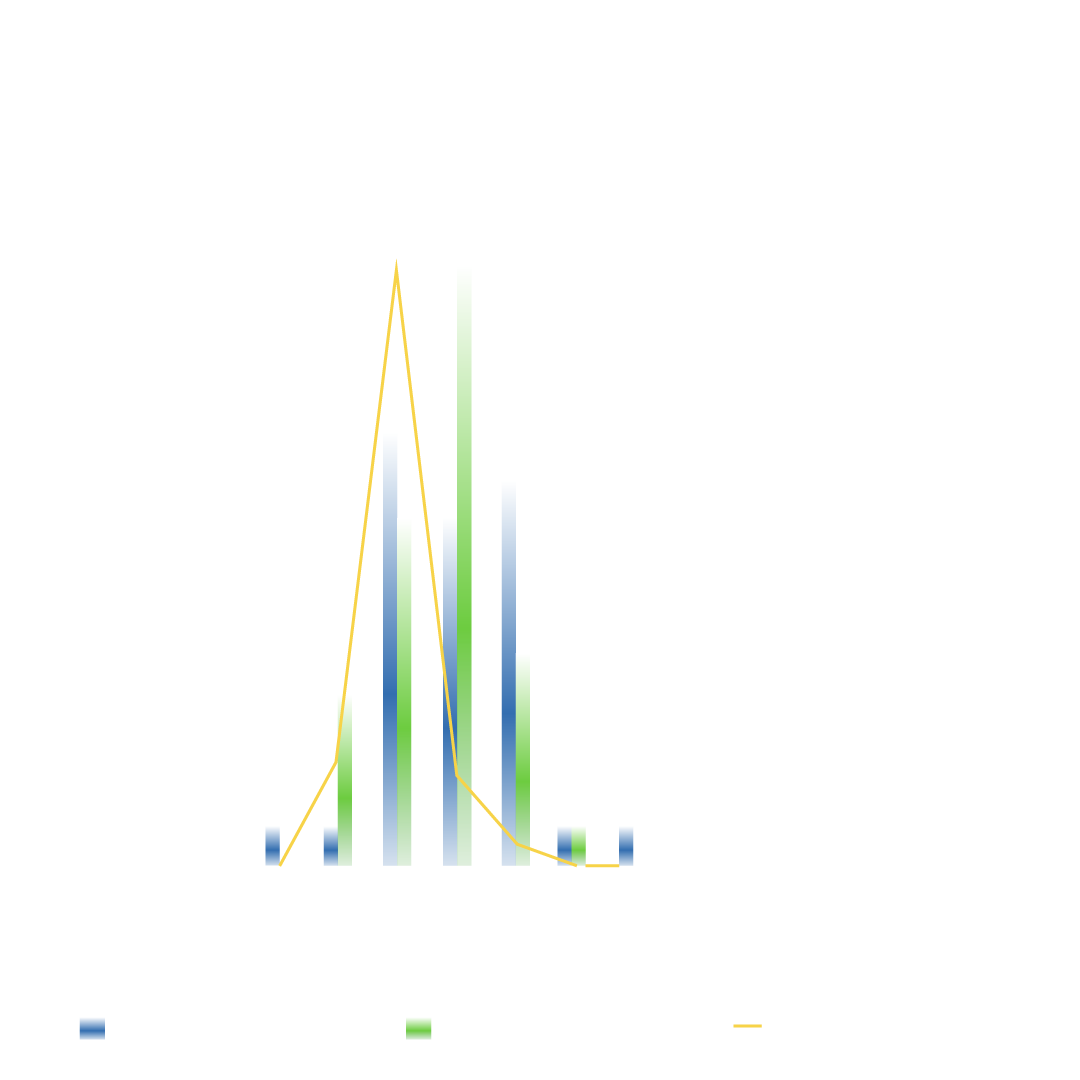

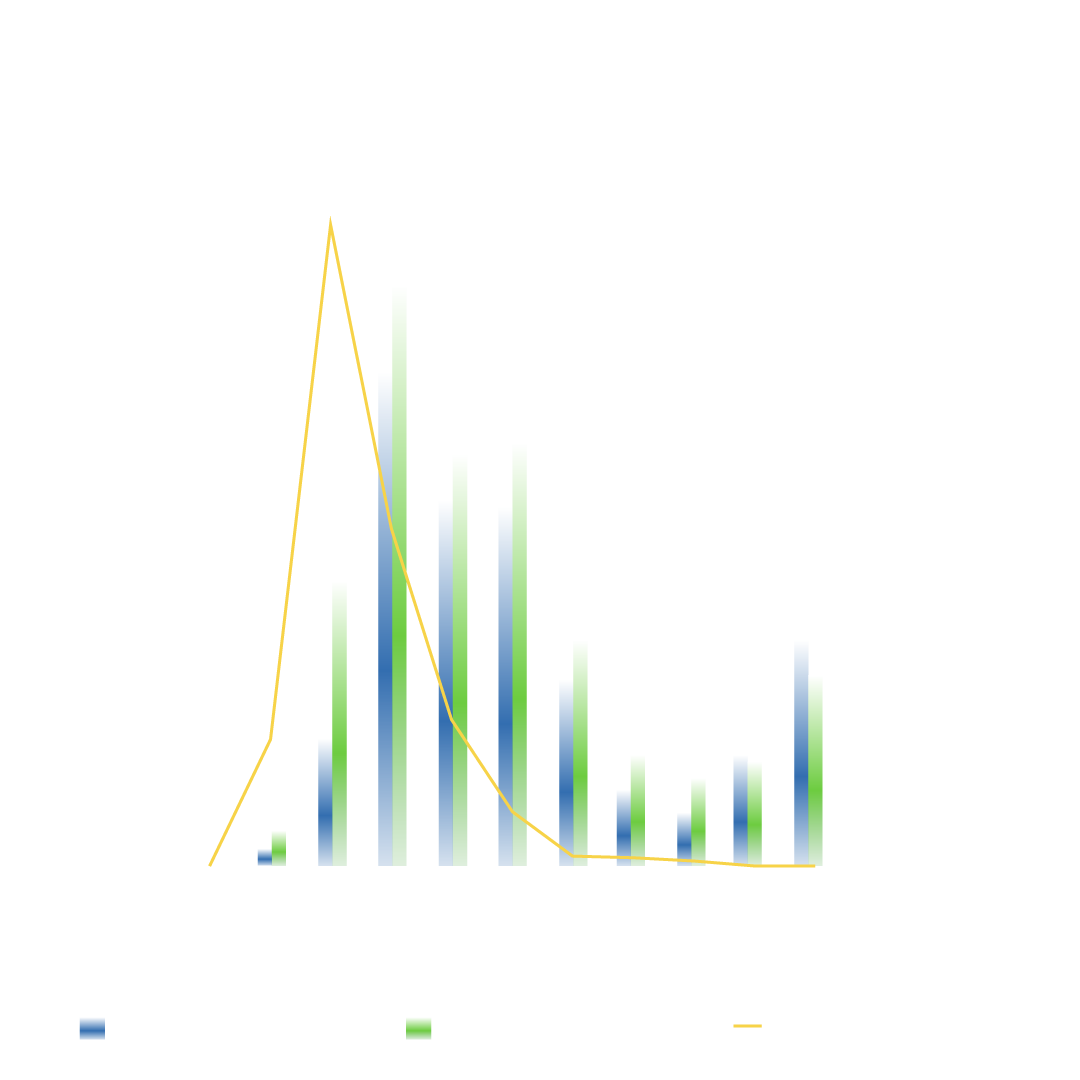

These graphs compare ZEV models available by price band for cars (left) and vans (right) in 2025 and 2026, with total model registrations by price (2025) overlaid for comparison. Since 2025, affordable ZEV models have increased, with the choice of car models in the sub-£30,000 price range more than doubling. Despite this, there remains a lack of ZEV model choice for cars priced below £30,000 where demand for ICEV typically sits. For vans, 63% of electric van models are priced above £40,000 despite most sales being for vans below that [EV Database, DfT, Manufacturer specs].

As ZEV technologies and supply chains are maturing, price reductions in entry-level electric cars and vans are falling and model capabilities are improving. For cars, the number of affordable models below £30k has increased from 25 to 55 models in 2026, with the £20-30k model segment again showing the fastest growth of any price bracket. In addition, the average range for sub-£30k models increased from 158 miles to 169 miles. There has also been a substantial increase in cars under £25k over the past year, from 12 models in 2025 to 22 models today [EV Database], while the new electric car grant reduces the effective price of some models by £1,500-3,750 [Gov.uk].

The affordable van market is showing an increase in available choices, but little sign of falling prices. There are now 26 models under £50k (17 in 2025), 12 under £40k (12 in 2025), and four models below £30k (one in 2025). The average range for van models reduced slightly to 201 miles in 2026, down from 206 miles in 2025, although most models are now capable of ultra-rapid charging speeds of at least 100 kW [Manufacturer specs].

![Business Leasing Demand[]@2x-100](https://roadtozero.co.uk/wp-content/uploads/2025/07/Business-Leasing-Demand@2x-100-scaled.jpg "Business Leasing Demand[]@2x-100")